Navigating the Mortgage Interest Deduction: What Homebuyers Need to Know in 2025

Buying a home is a major life milestone, and for many, the potential tax benefits associated with homeownership, like the mortgage interest deduction, are a welcome perk. However, if you're buying a home today, it's essential to understand that the ability to deduct mortgage interest has limitations, and it's not a blanket deduction for all homeowners.

Buying a home is a major life milestone, and for many, the potential tax benefits associated with homeownership, like the mortgage interest deduction, are a welcome perk. However, if you're buying a home today, it's essential to understand that the ability to deduct mortgage interest has limitations, and it's not a blanket deduction for all homeowners.

The Good News: You Can Still Deduct Mortgage Interest

The mortgage interest deduction is still a valuable tax benefit for many homeowners. It allows you to reduce your taxable income by a certain amount of the interest you've paid on your home loan throughout the year.

Here's where the limitations come in:

- Mortgage Debt Limits: The Tax Cuts and Jobs Act (TCJA) of 2017 reduced the amount of mortgage debt on which you can deduct interest for loans taken out after December 15, 2017.

a) For homes purchased after December 15, 2017, you can deduct interest on up to $750,000 of combined mortgage debt (including your primary residence and a second home). If you are married and filing separately, this limit is $375,000.

b) If you purchased your home on or before December 15, 2017, you can deduct interest on up to $1 million of combined mortgage debt ($500,000 if married filing separately).

- Home Equity Loan and HELOC Interest: The rules for deducting interest on home equity loans and lines of credit (HELOCs) also changed. For interest to be deductible, the loan funds must be used to buy, build, or substantially improve your primary or second home. You can no longer deduct interest on home equity loans used for personal expenses like paying off credit cards or taking a vacation.

- Itemizing Deductions: To claim the mortgage interest deduction, you must itemize your deductions on Schedule A (Form 1040) instead of taking the standard deduction. Since the TCJA significantly increased the standard deduction, many taxpayers now find that their total itemized deductions, including mortgage interest, do not exceed the standard deduction amount, making itemizing less beneficial.

What this means for you if you're buying today:

- Understand the Limits: Be aware of the $750,000 mortgage debt limit for loans taken out after December 15, 2017.

- Plan Your Home Equity Loan Usage: If you plan to take out a home equity loan or HELOC in the future, ensure the funds are used for eligible purposes (buying, building, or substantially improving your home) to potentially deduct the interest.

- Compare Itemizing vs. Standard Deduction: Carefully consider whether itemizing your deductions will benefit you more than taking the standard deduction, given the potentially higher standard deduction amounts. You can use tax software or consult a tax professional to help you determine which approach is best for your situation.

- Keep Good Records: Ensure you have the necessary documentation, like Form 1098 from your lender, to support your mortgage interest deduction claim.

In conclusion, while the mortgage interest deduction remains a valuable benefit, it's not a "hole mortgage interest" deduction. By understanding the now-permanent limitations and planning accordingly, you can make informed decisions and potentially maximize your tax savings as a homeowner.

Ready to explore homeownership?

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Is Your Connecticut Tax Bill Too High? New ATTOM Property Tax Data Exposed

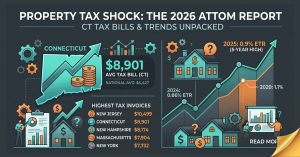

Facebook X Linkedin Is Your Tax Bill Too High? Breaking Down the Latest ATTOM Data If you’ve opened your mail recently and felt a bit of “tax shock,” you aren’t alone. The latest annual report from ATTOM Data Solutions, released yesterday (April 9, 2026), confirms that property taxes are reaching historic highs across the country-and […]

The Tale of Two Connecticuts: Hartford vs. Fairfield Market 2026

Facebook X Linkedin The Tale of Two Connecticuts: Decoding the Market Trends in Hartford vs. Fairfield Counties As we move through the 2026 real estate season, many of my clients are asking the same question: “Is it the right time to move, or should I wait?” The truth is, there isn’t just one “Connecticut Market.” […]

CT Real Estate Market Report March 2026: The Spring Surge Begins

Facebook X Linkedin Connecticut Real Estate Market Pulse March 2026 Report The Connecticut residential market continues to show remarkable resilience as we head into the second quarter of 2026. While sales volume has adjusted seasonally, pricing power remains firmly in the hands of sellers.Key Takeaway: Despite a 6.3% dip in the total number of sales […]

What Nobody Tells You About Buying in Hartford This Spring

Facebook X Linkedin The 2026 Connecticut Real Estate Pulse Statewide Trends & Local Insights | April 7, 2026 As we enter the second quarter of 2026, the Connecticut real estate market is standing at a crossroads. While global geopolitical tensions and oil price volatility are creating “inflation anxiety,” the Nutmeg State remains one of the […]

CT Millionaire Tax: How HB 5133 Impacts Connecticut Real Estate in 2026

Facebook X Linkedin The “Millionaire Tax” Wave: Is Connecticut the Next Domino to Fall? As Washington State moves to tax high-earners, all eyes are on Hartford. For Connecticut homeowners and investors, the 2026 legislative session could signal a major shift in property and income tax policy. For years, the conversation around “taxing the rich” was […]

How $3.8B in Defense Contracts are Shaping Connecticut Real Estate

Facebook X Linkedin Defense Contracts: A Multi-Billion Dollar Windfall for Connecticut Real Estate Connecticut’s “Aerospace Alley” just received a massive vote of confidence. Two major defense contract modifications were recently announced, totaling nearly $3.9 billion in combined value. The Big Numbers: $3.86 Billion Heading to CT The scale of these investments is staggering, anchoring thousands […]

From Snowy Strength to Economic Skepticism: The Great Divide in CT Real Estate

Facebook X Linkedin The February Resilience vs. The March Pivot: A Connecticut Real Estate Crossroads As March draws to a close, we find ourselves standing at the “great divide.” While the snow of February made showings a challenge, the data shows a market that was surprisingly robust-just before a wave of economic shifts changed the […]

© 2026 MoxiWorks

© CENTURY 21 2023 - 2024. All rights reserved. CENTURY 21®, C21® and the CENTURY 21 Logo are registered service marks owned by Century 21 Real Estate LLC. Franchisee Legal Entity Name (not the dba) fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each franchise is independently owned and operated. Any services or products provided by independently owned and operated franchisees are not provided by, affiliated with, or related to Century 21 Real Estate LLC nor any of its affiliated companies.